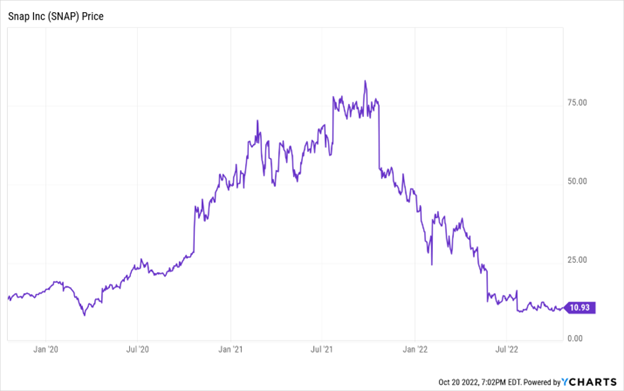

Everything seems to be falling apart at social media firm Snap (SNAP) right now. The company reported dismal third-quarter numbers last night and guided for even worse numbers next quarter. It seems the widespread digital ad recession is hitting Snap particularly hard.

Snap stock crashed more than 25% in response to the dismal report. It is now down more than 90% in just over a year.

{kind=link}

Let me repeat that: One of the world’s largest social media platforms has seen its stock price collapse 90% in a year.

I get it. Snap isn’t perfect. The company basically isn’t growing. Advertisers are pulling back spending. The company is a disaster right now.

But a 90% drop?! For a profitable firm with positive cash flows that’s still growing its user base by nearly 20% year-over-year?

That seems a bit overdone.

Indeed, in the chaos of the 90%-plus Snap stock collapse, we see an opportunity. That is, we believe Snap stock could rally 200% over the next year.

The intelligent investor sells high to optimists and buys low from pessimists. That’s why intelligent investors are probably buying Snap stock today. It’s also why they’ll probably sell Snap stock at much higher prices in a year to people that think it’s “going to the moon.”

Here’s a deeper look.

The Ad Recession Isn’t Forever

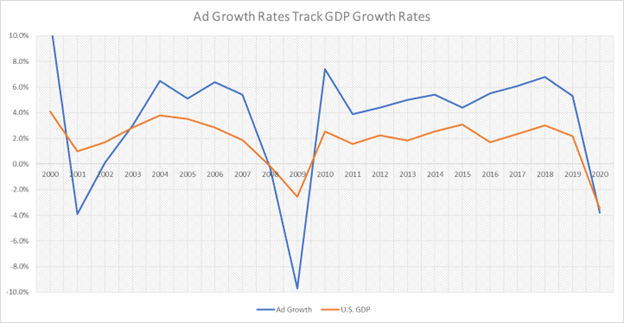

We’re in the midst of an ad recession right now, but it won’t last forever. And that’s the first big reason we like Snap stock at current levels.

The macroeconomic climate has deteriorated to a point where everyone is “battening down the hatches,” so to speak. In the marketing world, that means companies are slimming their ad budgets. This is not unusual. Typically, recessions and economic slowdowns cause ad spending to drop about 5% over the course of the year. Then, ad spending rebounds as the economy stabilizes. See the chart below.

{kind=link}

Right now, we’re in a slowdown. History says it should last about a year. Then, everything will rebound and we will enter a multi-year period of healthy ad spending growth.

Snap stock is crashing today as if the ad industry will never rebound.

That’s just silly. What Snap is going through right now is a totally normal ad-spending downcycle that will be over within a year. When it does end, Snap’s growth rates will rebound vigorously, and so will Snap stock.

So, if you’re trying to execute the old “buy low, sell high” strategy, this is your opportunity to buy Snap stock low. Everyone’s acting like this ad recession will last forever, but it will be over in a year.

The User Base Is Still Growing

Snap can’t control the macroeconomic climate or how much advertisers are willing to spend any given quarter. But the company can control the quality of its platform and how many users that platform attracts.

On that front, Snap is crushing it.

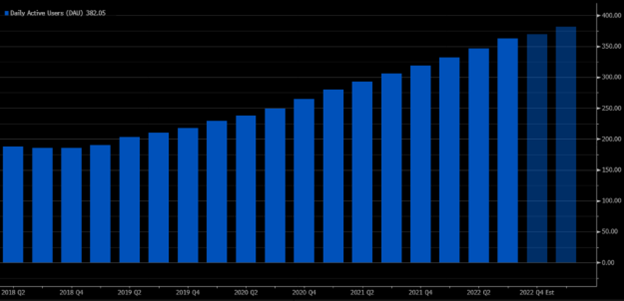

In the chaos of last night’s report, many missed the fact that Snap actually smashed estimates on daily active user (DAU) growth. DAUs rose18% in the quarter. Perhaps more impressively, while management said revenues will basically be flat next quarter (way below expectations), they also said that DAUs would clock in at 375 million (way above expectations and up 18% year-over-year).

{kind=link}

Said differently, Snap’s user base continues to grow at very impressive rates. Engagement trends remain very healthy with users spending a lot of time on the newly launched Discover and Spotlight features, as well as the redone Maps feature.

Users still love this app.

That’s important because ad dollars chase eyeballs. So, if Snap can maintain eyeballs (users) during this turbulent economic period, then a lot of those new ad dollars will flow into the Snap platform when the ad recession ends.

In other words, Snap’s ability to sustain robust user and engagement growth amid the 2022/23 downturn positions the company to rapidly reaccelerate revenue growth rates in 2023/24 as the ad recession turns into a new ad boom.

Soon enough, this will be a 10%-plus revenue grower again, and likely even a 20%-plus revenue grower. Yet, it’s priced as a no-growth firm – and that’s the last reason we love Snap stock here.

Snap Stock Valuation Is Dirt Cheap

Across the whole market, lots of high-quality tech stocks are going on “flash sale” right now, giving long-term investors a golden opportunity to buy amazing stocks at amazing prices.

Snap stock is a quintessential example of that.

The company is a strong one, with an experienced management team, a sticky product, a wide competitive moat, and a very profitable business model. That stock is now on fire-sale, trading more than two standard deviations below its historically “normal” sales multiple.

{kind=link}

Here are the numbers to huge upside over the next 12 months:

Snap will finish the year with 375 million DAUs. That number should grow by 10% per year for the foreseeable future, putting DAUs in five years at roughly 600 million.

Average revenue per user (ARPU) will clock in around $12.25 this year, after being at $13.75 last year. Let’s say ARPU drops 5% next year, consistent with a normal ad recession. That puts 2023 estimated ARPU at $11.60. After that, let’s say ARPU grows at a pretty normal 10% annualized pace, putting 2027 ARPU at $17.

A $17 ARPU on 600 million users implies $10.2 billion in revenues by 2027, under very conservative modeling assumptions. The business model lends itself to 30% EBITDA margins at scale – about $3 billion in implied EBITDA in five years. Our calculations say $3 billion in EBITDA should lead to about $2 billion in net profits, or about $1.25 in EPS in five years.

A very simple 20X forward P/E multiple on that implies a four-year forward price target for Snap stock of $25. Discounted by 10% per year, that puts our estimated 2023 price target for Snap stock at nearly $20 – which is almost triple the current value!

So, while Snap stock has collapsed 90% over the past year, the intelligent investor in us is telling us that it is time to buy from the pessimists who are investing by looking in the rear-view mirror.

By doing so, we think investors could make about 200% on Snap stock over the next year alone.

That’s a fabulous return. But it is far from the only high-quality growth stock we think has huge upside potential over the next year…

The Final Word on Snap Stock

Snap stock is part of a rare breed of stocks that emerge only about once a decade called “divergence stocks.”

Divergence stocks are stocks whose prices diverge dramatically from their fundamentals, such as revenues or earnings. For example, with Snap stock, the price has collapsed 90% from its peak in late 2021. But since then, revenues and profits have grown – and are expected to keep growing.

This is a classic divergence.

{kind=link}

Typically, when stocks have such huge divergences like this, they tend to snap back powerfully to their fundamental price lines. For Snap stock, that would imply a massive rally back above $50 over the next few years.

At the moment, we are witnessing dozens of these divergences emerge in the stock market. They are huge. And they are massive buying opportunities.

Our calculations imply that investors who buy top divergence stocks today stand to make more than 200% returns over the next year alone.

Snap stock is one such divergence stock. But it is far from our favorite.

Find out our favorite divergence stocks to buy right now.

On the date of publication, Luke Lango did not have (either directly or indirectly) any positions in the securities mentioned in this article.