The prospects for cybersecurity stocks vary greatly. During the pandemic, few companies that provided cybersecurity services supported working from home. In 2020, pandemic-related lockdowns forced these firms to enable staff to work remotely five days a week. Thus, significant investment in secure back-end technology infrastructure and networks took place. When the pandemic eased, companies wanted staff to come back to work. Thus, a new hybrid work environment has caused a massive shift in most companies’s cybersecurity needs.

On this environment, it’s important to consider which cybersecurity stocks are best-positioned to capitalize on this new environment. I’m going to look at mega-cap cybersecurity stocks, ranked by value and quality, as my metrics of choice.

{kind=link}

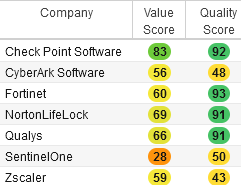

In the table above, cybersecurity stocks that have scores in green have good quantitative characteristics. For example, Stockrover found that firms with high quality have good historical returns on invested capital.

Looking at trends in the cybersecurity market, it’s important to favor the companies that protect customers from multiple points of entry, such as networks, cloud, and mobile environments. After gaining an understanding of these companies’ respective product offerings, as well as the potential upside based on the company’s recent quarterly results, readers can decide whether to invest. These seven cybersecurity stocks each differ, and I’ll dive into each below.

| NLOK | NortonLifeLock | $22.18 |

| CHKP | Check Point Software | $116.49 |

| FTNT | Fortinet | $55.49 |

| QLYS | Qualys | $139.10 |

| CYBR | CyberArk Software | $151.79 |

| S | SentinelOne | $23.58 |

| ZS | Zscaler | $151.03 |

NortonLifeLock (NLOK)

My top pick in this long list of cybersecurity stocks is NortonLifeLock (NASDAQ:NLOK). This major cyber player posted revenue growth of 2.5% year-over-year, bringing in $708 million this past quarter. In the company’s second quarter, it’s expected to post revenue in the range of $695 million to $705 million. One of the key catalysts I think can get the company here is its recent merger with Avast.

The U.K. Competition and Markets Authority recently approved NortonLifeLock’s acquisition of Avast. This approval paves the way for the combined firms to drive innovation in cyber safety.

As customers sign on to its platform, NortonLifeLock may communicate its service offering to them directly. For a few quarters, the company grew its user base for Norton 360 platform, which it sells on mobile. I think the company is likely to build on that positive momentum moving forward.

My key thesis with Norton is that a stronger product offering will increase customer retention. This is strategically important because Chief Financial Officer Natalie Derse expects macro-level headwinds will hurt traffic on its cyber safety website services. As the company works hard to increase visitor traffic to paying customers, profits will rise over time.

Check Point Software (CHKP)

Check Point Software (NASDAQ:CHKP) is the second-best cybersecurity stock on my list. That said, this isn’t a company without troubles.

Check Point recently reported billings below consensus estimates. Chief Executive Officer Gil Shwed said that this was because Check Point closed massive deals that last year that skewed results higher. For example, it benefited from a three-year deal last year that raised its billings significantly.

That said, Check Point has done an excellent job of preparing for the risk that the network security business slowing down. Fortunately, customers are shifting to the cloud and still need that type of security, which Check Point provides. In addition, Check Point has many loyal customers in Europe and Asia. It should post new customer additions over time. In the U.S., the company has plenty of growth avenues to attract new customers to its platform.

Among the key factors I think will drive customer growth is Check Point’s appealing product mix. The company’s CloudGuard for U.S. customers has been a hit, and Harmony offers customers the highest level of security for remote workers. Once corporations install CloudGuard or Harmony, the idea is that they might come back for more. Over time, I think this should result in higher revenue growth in upcoming quarters.

Fortinet (FTNT)

Fortinet (NASDAQ:FTNT) scored 60/100 on value and 93/100 on quality. CFO Keith Jenson said that the company faced order cancelations in the 4% or 5% range. Fortunately, the company has a strong backlog.

Looking ahead, CFO Jenson expects cancelation rates will fall. That’s based on the company studying the sources for its backlog. As a result, I expect cancellation rates to decline meaningfully.

Additionally, investors should expect shipments to strengthen in the next one or two quarters. Currently, demand is still outstripping supply, so if Fortinet’s backlog grows, this remains a positive development. I think the company has the right people in place to communicate with customers to retain their orders. Once fulfilled, Fortinent should report higher revenue from completed deals.

Fortinet’s diverse customer base is an attractive characteristic for shareholders. It has large and small business customers in its rolodex. As a result, the company has flexibility in its sales channels. For example, large enterprises may see bigger contractions in an economic slowdown. This could delay their purchasing of Fortinet’s products. However, the company may turn its attention to smaller customers during such a time.

Qualys (QLYS)

Qualys (NASDAQ:QLYS) is next on my list, with a relatively weak value score of 66/100. The company sells cyber risk management tools such as its Vulnerability Management, Detection, and Response tool, which may see declines should the economic slowdown continue.

That said, not all is lost for Qualys shareholders. The company may counter tougher market conditions by demonstrating the value of VMDR. In the last quarter, customers in Europe expanded their licenses with Qualys for VMDR. Many of these same customers are also adding Patch Management, and looking at the company’s Cybersecurity Asset Management product.

Qualys is helping customers realize more value in its product. Customers who run many virtual machines need cybersecurity tools to measure the risks of a cybersecurity attack. That’s where Qualys shines.

To enhance business growth, Qualys has formed new partnership programs and initiatives to develop its business. Unfortunately, the company did not give any details on what they are or how they are working out. Thus, I think investors should consider waiting for the company to post a stronger EBITDA margins and raising its guidance before committing to a position in QLYS stock.

CyberArk Software (CYBR)

CyberArk Software (NASDAQ:CYBR) scores 56/100 on value and 48/100 on quality (as shown above). This pushes CYBR stock toward the bottom of this list of cybersecurity stocks to buy. This company offers a range of identity security and access management products, which provide customers with security across various devices.

CyberArk sells its security as a platform, which provides customers with a complete security solution. This platform includes identity management products that span a client’s workforce to its machines. The transition to a SaaS model, or software as a service, is accelerating demand for endpoint privilege management. Demand remains strong for its EPM product, which suggests that CyberArk could post good results next quarter.

CYBR stock is priced to perfection at the moment. Thus, this stock really has no room to report weak renewal numbers or lower retention rates. Investors should watch the stock, and considering adding, should the company’s valuation improve. Expectations are that higher operating margins could be on the horizon in 2023. If these materialize, and the company’s stock price dips, I’d consider being a buyer.

SentinelOne (S)

SentinelOne (NYSE:S) enjoys a short sales cycle, which is reflected in the company’s high sales efficiency metrics as well as strong net retention rates. Still, after reporting a revenue increase of 124% year-over-year, the company found a way to lose money.

SentinelOne lost 20 cents per share on a non-GAAP basis. In the third quarter, the company will report revenue of $111 million. This is close to the $102.51 million posted in Q2. For the full year, the firm highlighted its revenue target, but did not put forward an earnings per share outlook.

In this severe bear market, investors are uninterested in technology firms that fail to post positive operating margins. Revenue may keep growing at impressive rates. Yet, each customer addition needs to lead to profitability.

Investors should worry that SentinelOne’s potential customers will cut unessential spending. While the firm will likely cut its expenses to adjust for weak market conditions, consider a stock that offers better value.

Zscaler (ZS)

Zscaler (NASDAQ:ZS) is last on this list of cybersecurity stocks for a reason. This is a company that’s likely to struggle to win deals as customers cut spending. The pervasive view that security and connectivity products are essential nondiscretionary budget items may not help this company in the near-term.

That said, the company might gain traction in the marketplace bank segment. The company is winning large deals for its hyperscaler solutions. Zscaler is helping customers understand its business value during the validation process. Unfortunately, many customers want Zscaler to quantify that value.

Zscaler risks losing larger deals as a result of the severe economic downturn. It will rely on its customer’s chief technology officer to explain the value of its cybersecurity product. In the interim, the company has $1.7 billion in cash. It will likely use this cash to invest in bringing its best products to market. In the short-term, the company needs to retain customers. In the next three to five years, many expect the company’s added applications in the public cloud could attract more business.

Investors are looking at near-term strength instead of long-term prospects. That might pressure ZS stock in the months ahead.

On the date of publication, Chris Lau did not have (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.